Searching for the top debt relief companies in USA can feel overwhelming. The debt relief industry is crowded, confusing, and often filled with bold promises that don’t explain the full picture. Meanwhile, consumer debt continues to rise across the country.

American household debt levels are way above where they should be. The Federal Reserve Bank of New York say that as of right now, total US household debt has hit $17.7 trillion. And then there’s the credit card debt at $1.1 trillion due to high interest rates and rising living costs. This shows the overall financial burden faced by people in the US, making it so difficult for many to maintain financial stability, and struggling to keep up with the minimum payments on their credit cards, medical bills, and personal loans.

Household debt

$17.7 trillionCredit card debt

$1.1 trillionRelief reduces

Up to 55% of debtIf you’re one of the many people struggling to pay off high-interest unsecured debt, you’ve probably seen many ads claiming fast results, huge savings, or “guaranteed” results. But debt relief doesn’t work like that. If you pick the wrong program, it can make your situation worse, not better.

What This Debt Relief Company Comparison Guide Covers

Instead of ranking companies based on advertising budgets or brand size, this guide helps you compare debt relief companies based on how they operate, who they’re best suited for, and what trade-offs consumers should understand before enrolling.

As Mark Joanis, CEO & Founder of Pathway Financial, often reminds clients:

“There isn’t a single ‘best’ debt relief company for everyone. The real difference comes down to how clearly a company explains your options, the risks involved, how they treat you, and whether their plan fits your financial situation.”

What Is Debt Relief and Who Is It For?

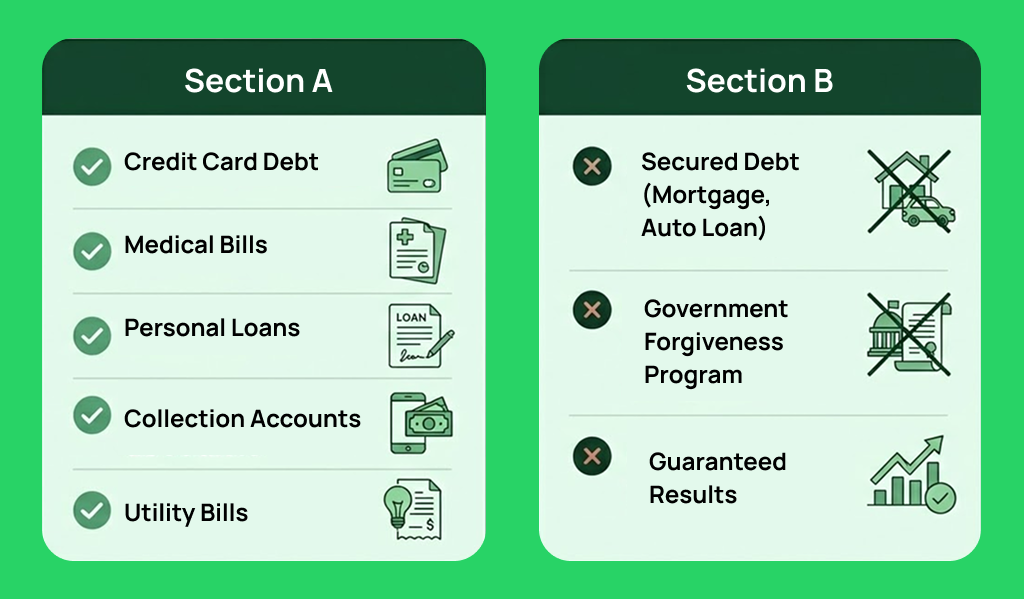

Debt relief is a term used to describe debt management programs designed to help people manage or resolve unsecured debts when repayment has become difficult due to some financial hardship. This debt management program helps people reduce or settle their unsecured debt by negotiating with creditors to settle debts for less than the actual amount they owe.

There are different types of unsecured debt, and the most common are credit card debt, medical bills, personal loans, collection accounts and utility bills (such as unpaid electricity, gas, or water bills, which can be included in debt relief programs).

Debt relief is typically explored when:

- Minimum payments no longer reduce balances

- Interest charges outpace income

- Cash flow becomes strained

- Financial stress affects daily life

What debt relief is not:

- It does not apply to most secured debts (such as a car loan or mortgage)

- It is not a government forgiveness program

- It does not guarantee reduced balances or credit protection

Debt relief programs do not require good credit for qualification, making them accessible to a wider range of consumers. Regardless, they can still have some credit requirements.

One of the biggest myths in the industry is that “debt relief” is a single solution. Instead, it includes multiple models, each suited for different financial situations. That’s why understanding your options before enrolling matters more than picking a brand name.

8 of the Top Debt Relief Companies in USA

There is no single “best” company for everyone. The right provider depends on your debt size, income stability, emotional comfort level, need for human guidance vs scale or whether repayment is realistic to your current financial status.

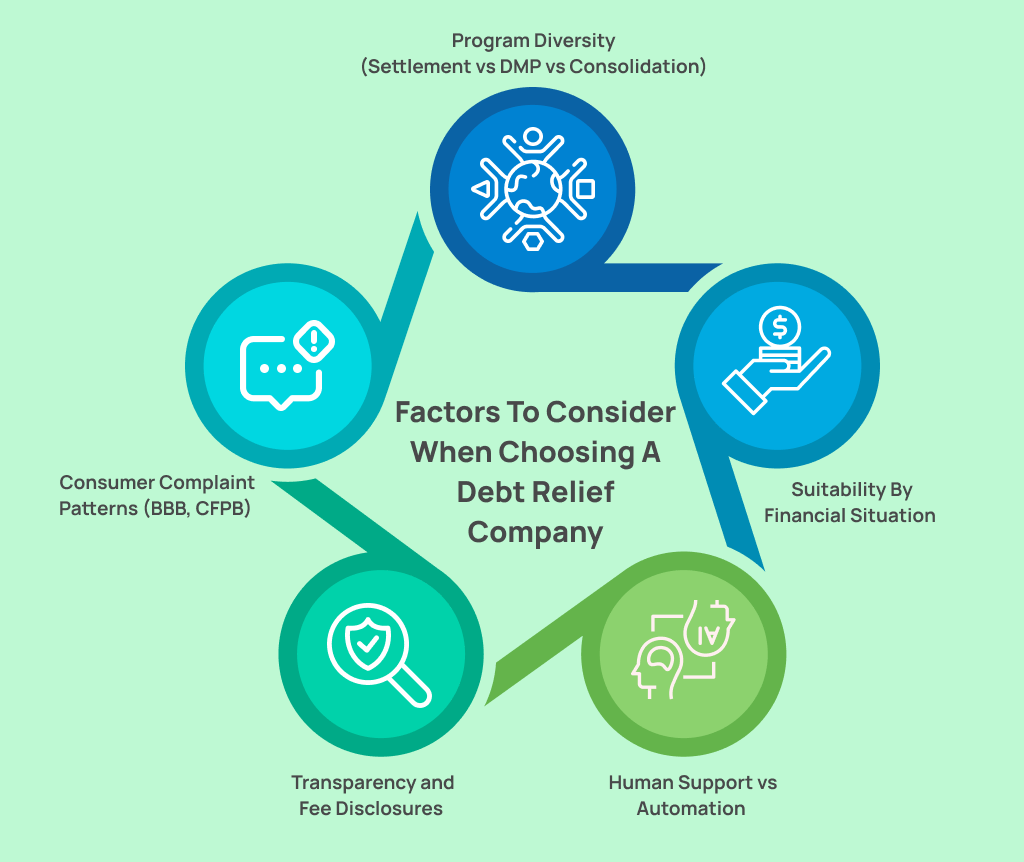

This evaluates providers based on:

- Transparency and fee disclosures

- Human support vs automation

- Program diversity (settlement vs debt management plan (DMP) vs consolidation)

- Consumer review patterns (Better Business Bureau, CFPB database)

- Suitability for different financial situations

Here are the top 8 debt relief companies we reviewed:

- Pathway Financial

- Verify Debt Solutions

- National Debt Relief

- Freedom Debt Relief

- Accredited Debt Relief

- TurboDebt

- Money Management International

- Apprisen

Many of these companies offer a free consultation to help you understand your options and determine the best path forward.

Comparison Chart: Debt Relief Guide

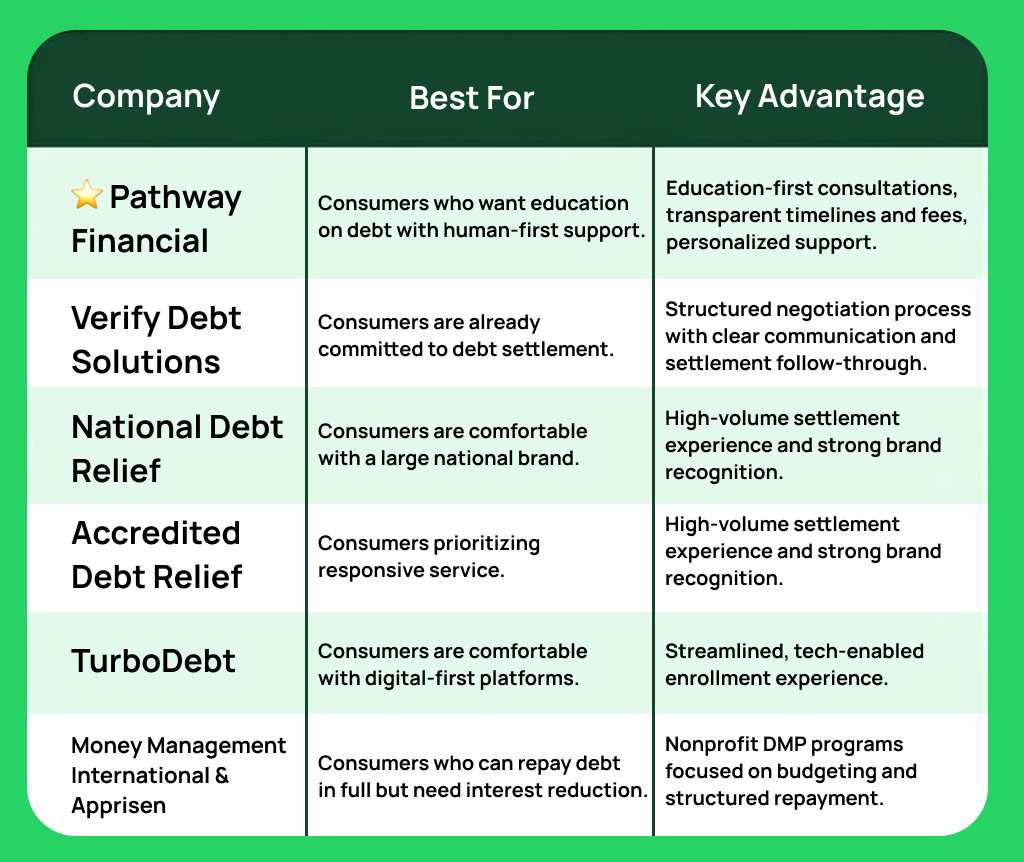

Pathway Financial

Best for: People who want to get their debt resolved with someone who takes the time to explain everything and guides them through the debt relief process before enrolling.

Why it stands out: Referred to by many clients as the best all-round debt relief solutions partner. Pathway Financial offers various debt relief plans and debt management programs. Their advocate education-first consultations and clear expectations around timelines, fees, and risks, supporting client’s long-term financial recovery.

Trade-off: Not the biggest organization in the industry. Its boutique model is intentionally built around client-focused support over high-volume enrollment and sales.

Verify Debt Solutions

Best for: People who already understand debt settlement and want structured negotiation assistance.

Strength: Clear process communication and strong follow-through in settlement-based programs. Verify Debt Solutions works to negotiate a settlement agreement with creditors with the goal of reducing the total amount owed through successful debt negotiations.

Trade-off: Primarily settlement-focused, may not suit consumers better positioned for counseling or consolidation.

National Debt Relief

Best for: People comfortable working with a large national brand.

Strength: Strong brand recognition and high volume of negotiated settlements.

Trade-off: National Debt Relief charges settlement fees, which are typically a percentage of the settled debt and are only charged after a successful settlement. Some clients report feeling like one of many accounts rather than receiving personalized support.

Freedom Debt Relief

Best for: People concerned about creditor escalation or legal exposure.

Strength: Offers structured legal support options within its debt management program. Freedom Debt Relief also helps clients achieve settled debt by negotiating with creditors to reduce the total amount owed.

Trade-off: Fees and program timelines vary significantly depending on debt size.

Accredited Debt Relief

Best for: People prioritizing responsive communication.

Strength: Strong customer service ratings and simplified structure.

Trade-off: Less emphasis on financial education depth compared to boutique firms in the market. Accredited Debt Relief may also charge a monthly maintenance fee as part of their debt management program, typically ranging from $10 to $50 per enrolled account.

Money Management International & Apprisen

Best for: People who can repay debt in full but need interest reduction.

Strength: Both Money Management International and Apprisen are nonprofit organizations focused on debt management plans (DMPs) and budgeting. As members of the National Foundation for Credit Counseling (NFCC), they adhere to industry standards for reputable credit counseling agencies.

Trade-off: Does not reduce principal balances, only interest and payment structure.

TurboDebt

Best for: Consumers comfortable with tech-enabled processes.

Strength: Streamlined online experience.

Trade-off: Less personalized advisory interaction compared to education-driven firms.

Best Debt Settlement Companies in USA

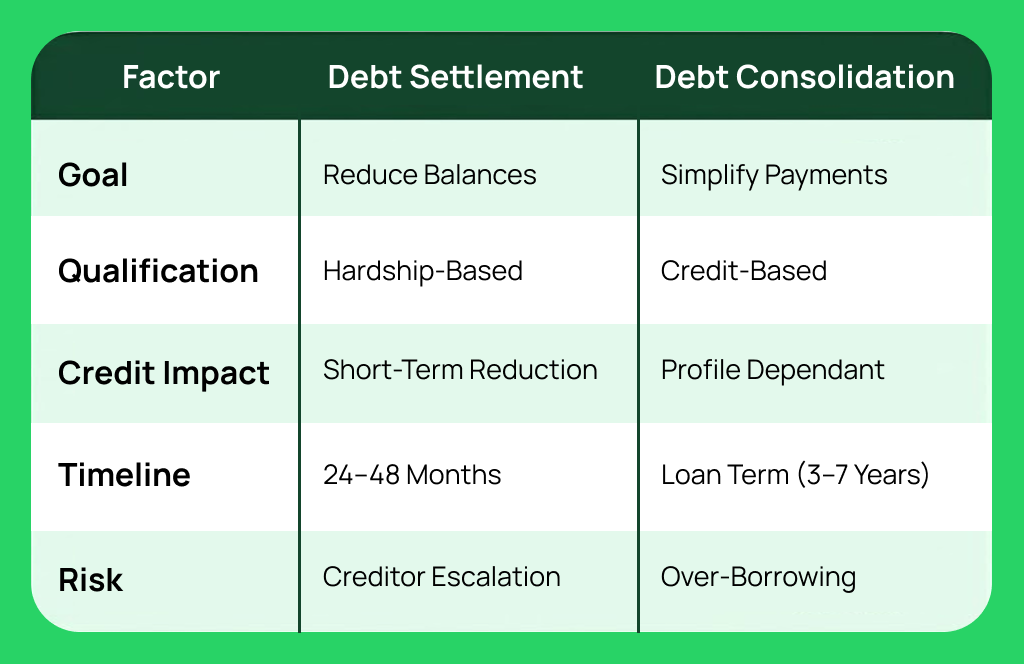

Debt settlement services companies negotiate with creditors to resolve unsecured debt for less than the full balance owed after hardship is demonstrated.

Under FTC rules, companies cannot charge upfront fees before achieving a settlement (FTC Telemarketing Sales Rule).

Typical program structure:

- Monthly deposits into a dedicated account

- A structured payment plan may be included to help clients manage their payments more effectively

- Fees charged after successful settlement

- Participating in a debt settlement program can help clients avoid late fees by ensuring timely payments through the program

- Potential short-term credit score impact

Research from the Money.com shows average settlement reductions often range between 25–50%, though results vary widely. Debt settlement programs aim to reduce the total debt owed, not just the monthly payment.

Among the best debt settlement companies in the USA, Pathway Financial stands out for education-first consultations and intentional support throughout the process, not just at sign up.

What is the Difference Between Debt Consolidation Loan vs Debt Settlement

Understanding debt consolidation loan vs debt settlement is important.

Debt consolidation loan combines multiple debts into one payment, often at a lower interest rate. By taking out a new loan to pay off existing debts, you can benefit from one monthly payment, which simplifies debt management.

The interest rate on your debt consolidation loan directly impacts your monthly payment and the overall cost of repayment. Lower interest rates can make your debt payments more manageable and reduce the total amount paid overtime.

According to Experian, debt management program like debt consolidation may improve credit mix but does not reduce total principal. Bankrate reports personal loan APRs often range from 8%–36% depending on credit.

Debt settlement program is typically more appropriate when repayment is no longer realistic.

What is the Best Credit Counseling Nonprofit?

The best credit counseling nonprofit agencies offer Debt Management Plans (DMPs).

Organizations like Apprisen and Money Management International are some of the best. Most operate under NFCC standards and offer a specific DMP (debt management plan) structure:

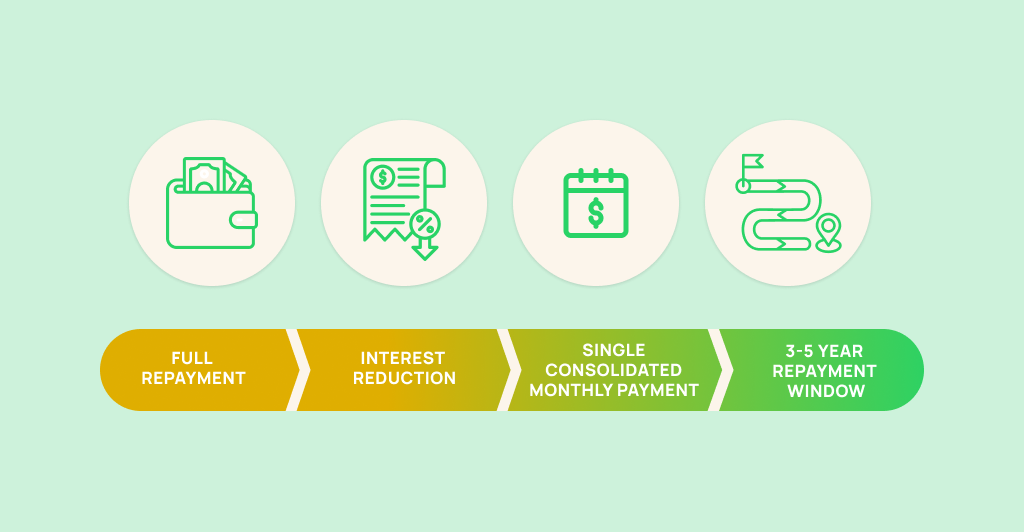

DMP structure:

- Full repayment is usually expected

- Negotiated interest reduction

- One consolidated monthly payment

- 3–5 year repayment period is typical

A steady income is typically required to qualify for a debt management plan, as it demonstrates the ability to make regular payments.

These are limited because they don’t reduce the principal debt amount and are best for consumers with steady income who can repay most of what they owe.

Comparing Credit Counselling vs Consumer Proposal

Comparing credit counselling vs consumer proposals aren’t always relevant because it’s a Canadian legal insolvency process and does not apply in the United States.

U.S. equivalents include:

- Credit counseling (DMPs)

- Debt settlement

- Bankruptcy (Chapter 7 or 13)

Consumers often confuse cross-border terminology, verifying jurisdiction matters before enrolling in any program.

What are the Best Debt Relief Companies for Your Situation?

Evaluating your repayment strategy, such as whether to use the debt avalanche method or debt snowball method can also help determine if debt relief or another option is best for your situation.

Here are some tips when choosing the debt relief company:

- Always verify and check Better Business Bureau complaint patterns, CFPB complaint database records, fee disclosures and written program details.

- You should avoid companies that: guarantee results, downplay credit impact, and pressure immediate enrollment.

Common Questions About Top Debt Relief Companies in the USA

Is debt relief for Americans legitimate?

Yes, debt relief is a legit financial help option in the U.S. for people who are struggling with debt. Just make sure to work with a reputable debt relief company that follows FTC regulations and is upfront about the risks, fees, and alternatives.

How do debt settlement companies work?

Debt settlement companies negotiate with creditors to resolve unsecured debts for less than the full amount owed. It is usually after accounts fall behind due to hardship. Clients usually make monthly deposits into a dedicated account while negotiations are ongoing, and once a debt is settled, it is reported as “settled” or “paid less than the full amount” on your credit reports.

Are debt settlement companies a good option?

Yes, it is. They can be a good option if you really can’t pay off your unsecured debts due to financial hardships. Debt settlement companies offer a safer debt relief solution to resolve debt by negotiating with creditors to reduce total balances and create a manageable path forward compared to ongoing delinquency.

How long does a debt relief order take to process?

Most debt settlement programs usually take around 24 to 48 months to complete, depending on how small or big the debt is and how willing the creditors are to work with the company. Since each debt is different, the program’s completion timeline may vary and may take shorter or longer.

Making a Choice for Debt Relief Services

When debt relief options feel rushed, overly technical, or sales-driven, it’s easy to lose confidence. And when that happens, many people either delay acting out of fear or enroll in programs they don’t fully understand, only to regret the decision later.

Finding the right debt relief company is about choosing a partner who is transparent, honest, and takes the time to explain what’s happening, why it’s happening, or what options realistically make sense for you.

That’s where we stand out. We treat debt relief as a guided decision-making process. You’ll work with real, experienced debt specialists who will help you explore programs that actually fit your current financial situation.

What Makes the Best All-Around Debt Relief Company

Clear explanations before commitment

You’ve walked through how debt relief programs work, what the process looks like, and what to realistically expect based on your specific circumstances—before any enrollment decisions are made.

Honest discussion of risks, timelines, and alternatives

Potential credit impact, timelines, fees, and trade-offs are explained upfront. This includes how settled debts may affect your credit report, possible tax consequences, and when alternatives like a debt management plan, or speaking with a bankruptcy attorney may be more appropriate.

Education-led consultations without pressure

There’s no urgency to enroll. You’re encouraged to ask questions, take time, and make decisions at your own pace without pressure.

Consistent human support

You work with real people throughout the process, not rotating call-center agents or automated systems. And dedicated support continues across your enrolled debt, not just at signup.

Focus on informed consent

Enrollment is only recommended when debt relief aligns with your financial situation and long-term goals. We prioritize understanding and consent over quick enrollment.

Commitment to industry standards

Memberships in international associations, such as the International Association of Professional Debt Arbitrators (IAPDA), are highly valued in the debt relief industry for upholding ethical and professional standards. These affiliations help ensure companies adhere to best practices and maintain trustworthiness in their services.

So far, we’ve helped people navigate complex debt decisions across a wide range of unsecured debt situations, including:

- Credit card debt with high interest and multiple accounts

- Medical debt from hospital bills, healthcare expenses, or collections

- Unsecured personal loan debt with limited repayment flexibility

- Accounts already in collections or charged off

- Multiple overlapping debts with competing monthly payments

- Delinquent or past-due balances at risk of further collection activity

- Situations where debt repayment no longer aligns with income or capacity

Unlike many debt relief companies that focus on fast enrollment or headline savings, we don’t treat debt as a one-size-fits-all problem. Every conversation starts with understanding your situation and walking through all relevant options, including times when debt relief may not be the right move.

We do not promise to make everyone debt free. Instead, the focus is on informed decisions, realistic expectations, and long-term financial confidence, not pressure or guarantees.

Ready to Explore Debt Relief Options?

Try out our debt relief calculator to estimate how much you can save from our debt relief options and schedule a free consultation with experienced debt specialists. Learn how debt relief works, whether it makes sense for your current financial status, and what alternative programs may be available if it doesn’t.

Take the first step toward a clearer path to becoming debt-free today.

- US Household Debt Climbs to $17.7 Trillion – Federal Reserve

- Credit Card Debt Hits Record High

- FTC Telemarketing Sales Rule

- How Debt Relief Impacts Your Credit

- How Much Does Debt Settlement Really Save?

- What Is Debt Management?

- Average Personal Loan Rates

- Better Business Bureau (BBB)

- International Association of Professional Debt Arbitrators (IAPDA)