Your income comes in. Your credit card bills go out. Somehow, it still feels like you’re not making real progress. If that sounds familiar, you’re not alone.

This situation plays out for millions of Americans every day. Many people find themselves stuck under growing unsecured debt, unsure which step to take next.

When people begin exploring solutions, they’ll see overwhelming information about the different debt relief companies and their services, programs, and approaches. But, understanding how these options work and how they differ can make it much easier to choose a solution that truly fits your situation.

US Households Carry

77%+ Unsecured DebtAverage Credit Card APR

Exceeds 20%Americans Experiencing

Ongoing Debt Stress: 1 in 3Comparing Debt Relief Companies Is Key

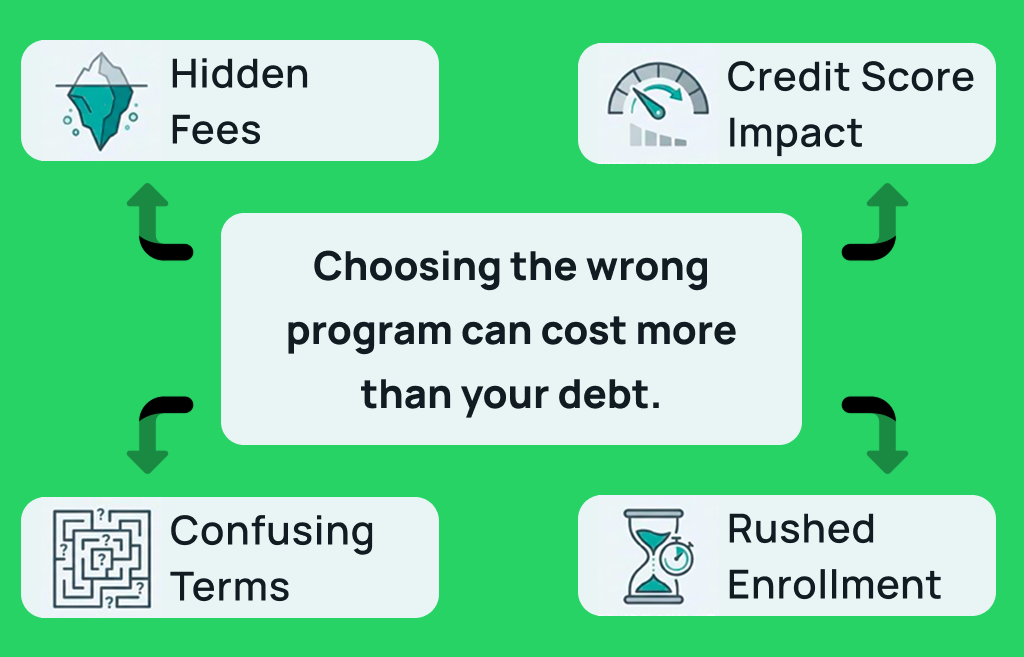

Across the industry, some companies prioritize speed, advertising, or enrollment volume not long-term fit. Choosing the wrong program can cost more than the debt itself, both financially and emotionally.

The wrong structure can lock you into fees that don’t align with your income, impact your credit more than expected, leave you feeling rushed, confused, or unsupported, and prevent you from exploring alternatives that may have been a better fit.

This guide helps you compare debt relief companies based on structure, transparency, use case, and support model, so you can understand which option truly makes sense for your situation.

Mark Joanis, the CEO & Founder of Pathway Financial, says that throughout the decision-making process:

“Most debt problems don’t come from a lack of effort – they come from a lack of information. When people understand their options, better decisions follow, and they’ll see a path out of debt”

How a Debt Relief Program Works

Before you compare debt relief companies, you need to understand how a debt relief program works for each type they come in.

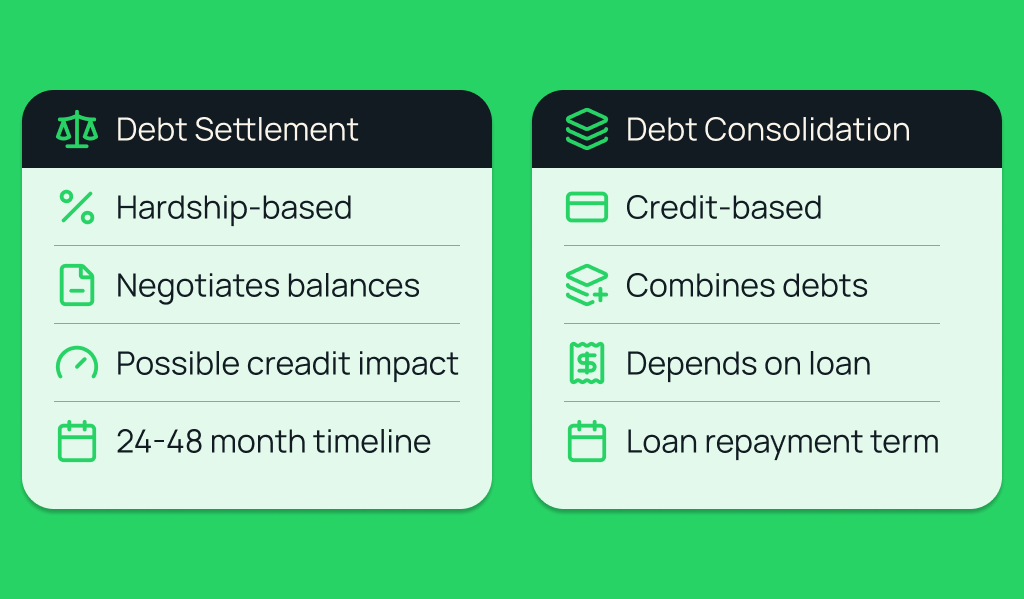

Debt Settlement (Hardship-Based Relief)

You may want to consider debt settlement if you can no longer realistically repay your unsecured debt in full due to financial hardship. A debt settlement company negotiates directly with your creditors on your behalf and may advise you to stop paying your creditors temporarily to strengthen your negotiation position.

Here’s how it generally works:

- You make monthly deposits into a dedicated account.

- The debt settlement company negotiates with creditors.

- Settlements may resolve balances for less than the full amount owed.

- Fees are charged only after a successful settlement (as required by the FTC Telemarketing Sales Rule).

- Fees are typically charged as a percentage of the settled debt.

Because accounts may become delinquent during negotiations, credit impact is possible, especially in the early stages. Most settlement programs take approximately 24–48 months, depending on debt size and creditor participation. Debt settlement is usually appropriate when minimum payments no longer reduce balances; interest outpaces income and you’re already falling behind your payments.

PLEASE NOTE: You should consider this option carefully as debt settlement services can have a negative impact on your credit score.

Debt Consolidation (Credit-Based Restructuring)

Debt consolidation involves taking out a new loan to combine multiple debts into one payment. This new loan is often called a “consolidation loan” or “debt consolidation loan”. This may include personal loans as an option for borrowers seeking to streamline repayment and potentially secure a lower interest rate. However, it does not reduce the amount you owe.

According to Experian, personal loan APRs typically range from 8% to 36% depending on credit profile. Experian also notes that consolidation of loans requires enough credit score to make it worth it.

Debt consolidation works best when your credit is still strong, income is stable, and the problem is interest rate, not total balance. If repayment is still realistic, a debt consolidation loan may be an appropriate choice. But if not, settlement may be a better debt relief option.

Debt Management Plans (Nonprofit DMPs)

Nonprofit organizations and credit counseling agencies such as Money Management International and Apprisen offer Debt Management Plans (DMPs) and counseling services. These programs do not reduce principal balances, but instead:

- Repay the full principal

- Negotiate lower interest rates

- Consolidate debts into one monthly payment

- Typically run 3–5 years

- Charge a typical monthly fee

- One-time enrollment fee for setting up and maintaining the plan

They’re best suited for consumers who have stable income, can repay most of what they owe, and need interest reduction and structured budgeting.

Types of Debt Relief Companies

Now that you understand the main program structures, it’s important to understand how companies themselves are structured.

Not all debt relief companies operate the same way. The market includes both top debt relief providers known for their strong reputations and proven results, as well as other debt relief companies that may differ in experience, transparency, fees, and service models.

Large National Debt Settlement Firms

These firms often focus on operational efficiency and scale. Large national firms also promote their high customer satisfaction ratings from sources like the Better Business Bureau and Trustpilot as a key selling point. They also have:

- High volume, large scale

- Strong brand recognition

- Standardized processes

- Less personalization

Mid-Sized Negotiation-Focused Companies

These companies often prioritize structured negotiation processes and:

- Balance between scale and service

- Often similar settlement models used by many settlement companies

- Moderate personalization

Nonprofit Credit Counseling Agencies

These are best for consumers who can realistically repay their balances in full and:

- Focus on repayment and interest reduction

- Lower risk, slower outcomes

- No balance reduction and usually centered around a debt management plan with credit counselors who provide professional guidance and require financial discipline from participants.

Boutique, Human-First Advisory Firms

Boutique firms tend to prioritize trust, transparency, and understanding, while large firms prioritize efficiency and scale. They are also:

- Smaller scale, higher clarity

- Education-first approach

- Personalized guidance from real debt relief partners

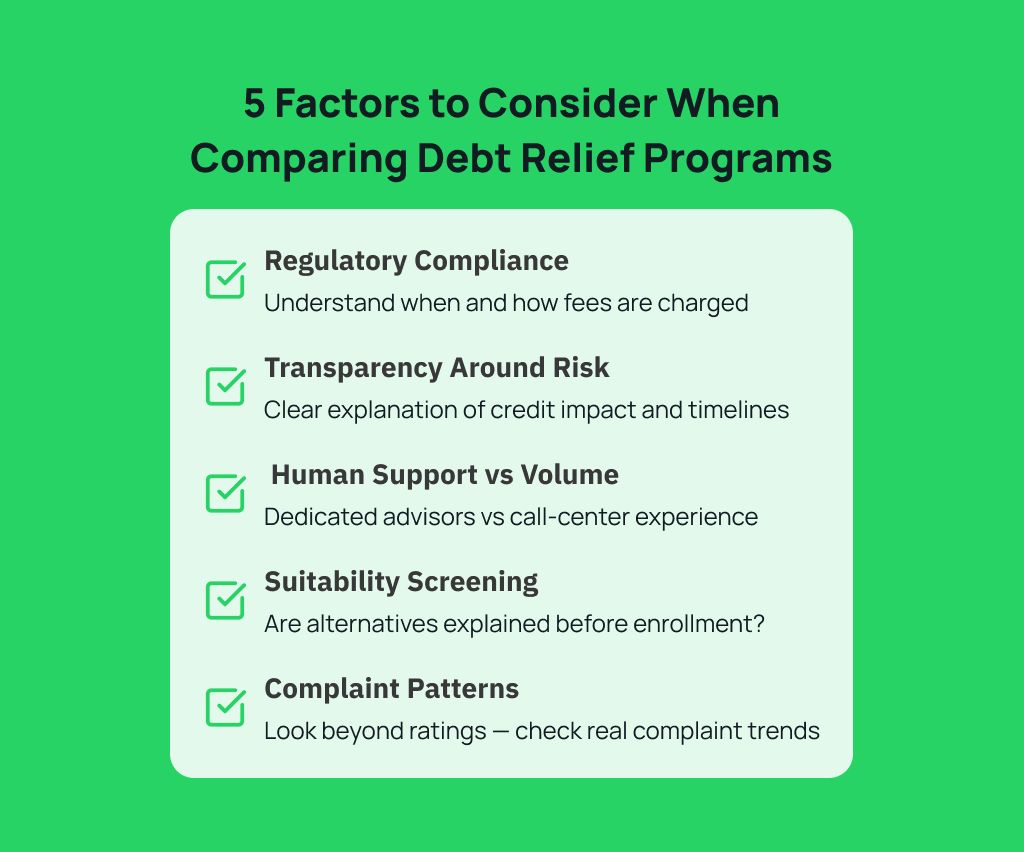

5 Factors to Consider When Comparing Debt Relief Programs

Once you understand the models, the next step is knowing the factors to consider when comparing debt relief programs. It’s not just about how much you can save. It’s about being informed about the company structure, its transparency, reviews, and whether the program they offer is the right fit for you.

Remember, it’s important for you to understand what it means to be working with a debt relief company, how it may affect your credit, eligibility requirements, and the types of debt or how many accounts can be included, so you can make informed decisions about your financial future.

1. Regulatory Compliance

The FTC prohibits debt settlement companies from charging fees before achieving a settlement (FTC Telemarketing Sales Rule).

You should clearly understand hen fees are earned, how they are calculated, and whether a dedicated account is used. If that explanation feels unclear, that’s a red flag.

2. Transparency Around Risk

Debt relief can impact credit scores. Forgiven debt may have tax implications in certain cases (IRS Form 1099-C guidance). Responsible companies explain the following because education reduces regrate:

- Credit report & score impact

- This includes negative marks that may remain for up to seven years

- Mostly incur through debt settlement or bankruptcy

- Impacting future loan approvals and financial opportunities

- Timeline expectations

- Settlement variability

- Alternatives available

3. Human Support vs Volume Enrollment

Some national firms operate at scale. That often means rotating representatives, scripted consultations, and high enrollment volume. Boutique firms often prioritize dedicated advisors, ongoing continuity, and Personalized screening There’s nothing inherently wrong with scale, but support style matters if you value clarity.

4. Suitability Screening

A strong company doesn’t enroll everyone. If they did and never discuss alternatives, that should concern you. They should ask:

- Can you realistically repay through a DMP?

- Do you qualify for consolidation?

- Would bankruptcy consultation be more appropriate?

5. Complaint Patterns

The CFPB Consumer Complaint Database provides insight into complaint trends and the Better Business Bureau tracks complaint resolution patterns.

Instead of just reading star ratings, review fee disputes, communication breakdowns, and timeline complaints. The patterns matter more than just positive testimonials.

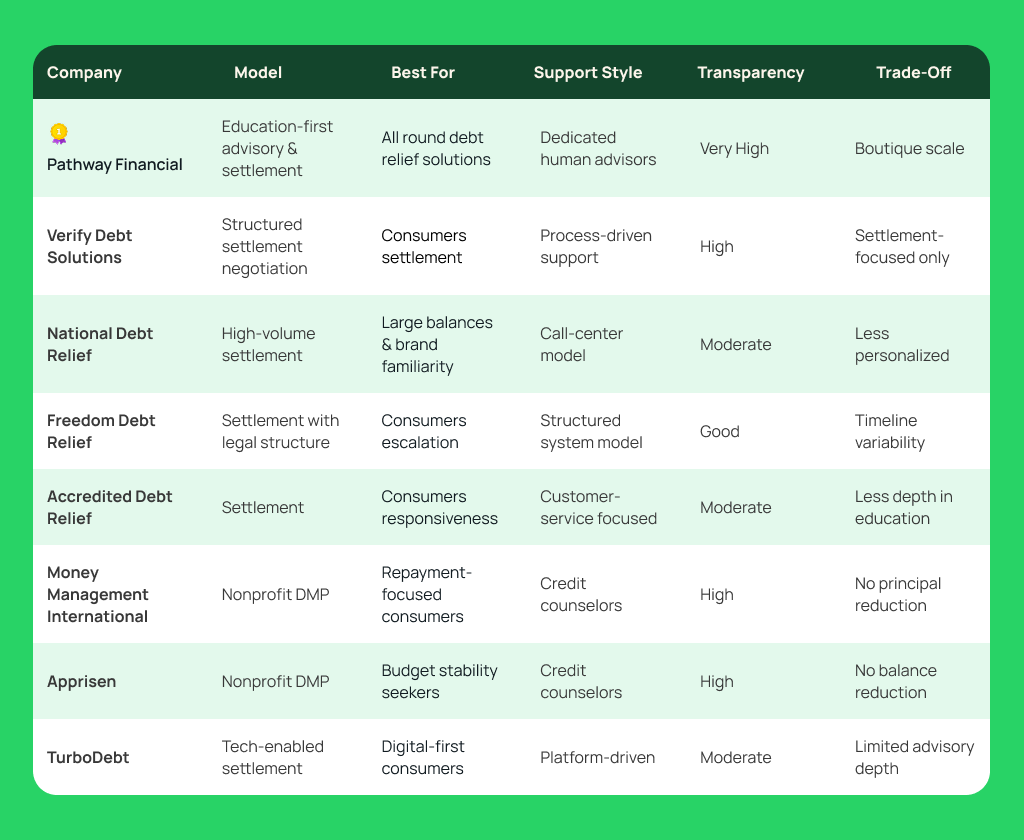

Debt Relief Program Comparison Chart

We’ve broken down your options in this debt relief program comparison chart below. Depending on your goal, principal, timeline, credit score, income, and risk tolerance, there is a debt relief program that’ll fit you best.

Debt Management Program Comparison Based on Risk Tolerance

Another way to consider a debt management program comparison is based on the level of financial and credit risk that they come with.

- Low risk, full repayment → DMP

- Moderate risk, interest reduction → Consolidation

- High hardship, need reduction → Settlement

- High risk, high reward → Debt forgiveness (negotiating with creditors to reduce the total owed; can impact credit and may have tax implications)

- Legal restructuring → Bankruptcy consultation (involves a formal legal process with court proceedings, asset evaluation, and court approval)

Comparing companies without understanding your risk of tolerance leads to poor alignment. Here are the top debt relief providers:

Debt reduction varies based on creditor participation, hardship documentation, and funding capacity. These companies help clients manage their total debt and work toward debt payoff through structured plans and settlement strategies.

Choosing the Best Company for Debt Relief

There is no single best company for debt relief for everyone. The best debt relief companies are those that help clients achieve financial freedom through transparent and supportive services.

The best fit depends on debt size, income stability, credit condition, emotional comfort level, and desire for human guidance.

Some companies focus on speed and enrollment volume. Others focus on repayment-only programs. A smaller group focuses on education, screening, and long-term clarity before enrollment. Certain firms are more balanced across structure, support, and transparency like Pathway Financial.

Many clients have referred to Pathway Financial as the best all-around debt relief company because of its balanced, education-first approach. They’re the best for consumers who want clarity, intentional guidance, and a full understanding of their options before making a commitment.

Rather than emphasizing speed or aggressive enrollment targets, we prioritize understanding, helping clients choose the right solution for their specific situation, even if that means exploring alternatives outside settlement. For many consumers, that balance of structure, transparency, and human guidance is what makes the difference.

What to Look for in a Reliable Debt Relief Company

- Clear explanations before commitment

You’re guided through how debt relief programs work, what the process involves, and what you can realistically expect based on your situation.

- Honest discussion of risks, timelines, and alternatives

You’ve walked through the full picture before anything moves forward. That includes potential credit impact, timelines, fees, and possible downsides. It also explains how settled debts may appear on your credit report, potential tax consequences, and how forgiven debt amounts could create tax implications.

- Education-led consultations without pressure

There’s no urgency to enroll. You’re encouraged to ask questions, review your options, and make decisions at your own pace.

- Consistent human support

You work with real people, not rotating call-center agents or automated systems. Our team stays involved and acts as a trusted support system throughout the process.

- Focus on informed consent

Enrollment is only recommended when debt relief aligns with the individual’s financial situation and goals, including whether settlement, a debt management plan, or alternatives like consulting a bankruptcy attorney might be more appropriate in complicated or extreme cases.

- Commitment to industry standards

Memberships in international associations, such as the International Association of Professional Debt Arbitrators (IAPDA), are highly valued in the debt relief industry for upholding ethical and professional standards. These affiliations help ensure companies adhere to best practices and maintain trustworthiness in their services.

Common Questions When Comparing Debt Relief Companies

What is the best debt relief option?

There is no single best option for everyone. The right debt relief solution depends on your income stability, total debt amount, credit condition, and whether repayment is realistic or financial hardship has already occurred.

Which debt relief option is considered the most aggressive?

Debt settlement is usually the option that people view as the most intense because in most cases it’s about negotiating the amount you owe after things have gone from bad to worse with your finances.

Do debt relief companies offer support after program completion?

Some of them will, especially if they’re really focused on helping you achieve long-term financial stability. Having that extra guidance can make a big difference in terms of recovery and planning for the future.

How do debt relief programs help individuals with high unsecured debt?

They give people a clear plan to follow, help you negotiate with your creditors, and give you a sense of what you’re looking at — and that can be a huge stress relief when you’re dealing with a bunch of different debts.

What are some debt relief options available to me?

Common options include credit counseling, debt consolidation, debt settlement, and bankruptcy alternatives. The right choice depends on your income, debt type, and overall financial situation.

What Is the Difference Between Debt Relief and Debt Consolidation?

The difference between debt relief and debt consolidation is that consolidation is just one type of debt relief option and financial tools available to consumers. Debt relief is a process that gets consumers out of debt, and while debt consolidation is part of it, there are many other debt relief options as well as debt settlement and negotiation.

Finding the Right Debt Relief Partner for Your Situation

When debt solutions feel rushed, confusing, or overly technical, it’s hard to feel confident about any decision. And when that happens, people usually do one of two things. They avoid dealing with the debt altogether, or they enroll in a program they don’t fully understand and regret it later.

Getting control of your debt starts with working with a debt relief partner who takes the time to help you understand your options. That’s where we make a difference.

When you work with us, you’re talking to real debt specialists who walk you through how debt relief works, what the process looks like, and whether a program makes sense for your situation before recommending any next steps.

So far, we’ve helped people with complex debt relief decisions and work toward financial stability across a wide range of unsecured debt situations, including:

- Credit card debt with high-interest revolving balances

- Medical bills and healthcare-related debt

- Unsecured personal loans with high interest

- Accounts that have been charged off or sent to collections

- Multiple overlapping debts with competing monthly payments

- Past-due or delinquent accounts facing collection activity

- Situations where monthly payments no longer match someone’s income or financial capacity

We don’t treat these situations as one-size-fits-all problems. Every conversation starts with understanding your situation and walking through your options, including times when debt relief may not be the right move.

We do not promise to make everyone debt-free. Our focus is on helping you understand your options, set realistic expectations, and make confident financial decisions without pressure or unrealistic guarantees.

Take a Closer Look at Your Debt Relief Options

Check out our debt relief options and schedule a free consultation with experienced debt specialists. Learn how debt relief works, the different debt relief approaches available for you and see how they compare based on your debt type, income stability, and financial goals.

Start moving toward a clearer path to debt freedom today!